The investor panel recording on the water innovations (Jan.26, 2024). Thanks to all the panelists for the great conversation and the chat record is here.

A suggestion from Paul Burgon, Exit Ventures – (he has a background in running the North American division of a public European water tech company and also being on their board)

My observations: I agree with your investment opportunities points. One clarification I would add: startups should not focus on customers in the municipal water sector, it is a complete mismatch. Municipal water operators are extremely risk averse and they won’t be interested in a startup’s new technology until it has seen years of use and testing, unless the municipality is almost desperate. They are very rarely desperate. So, startups should focus on industrial water testing and reclamation rather than municipal. The industrial segment will be much more open to trying newer technologies with a strong ROI and so startups can be much more successful in the industrial segment.

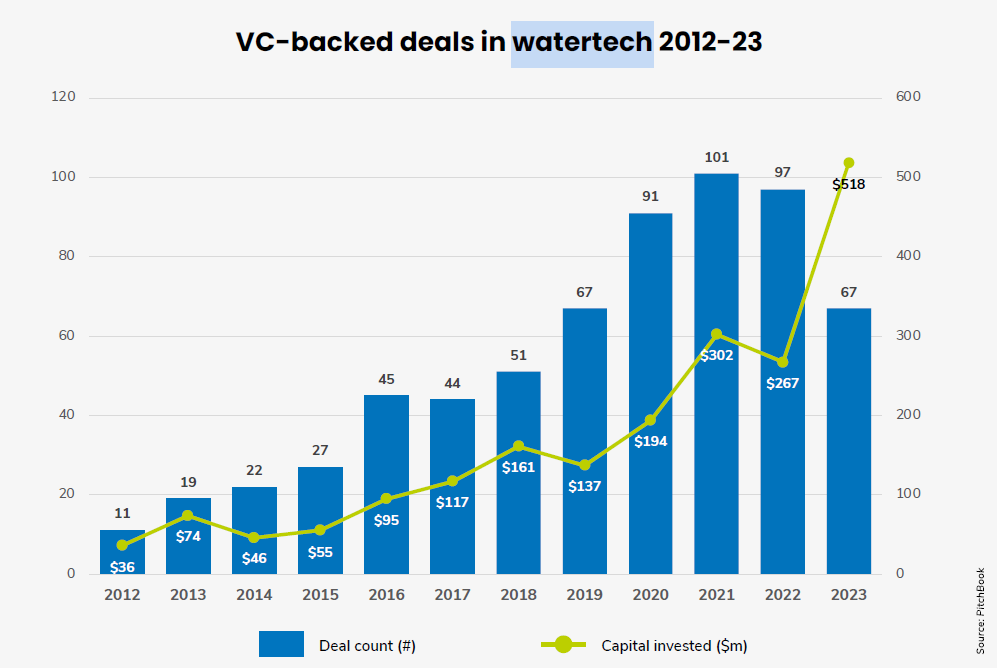

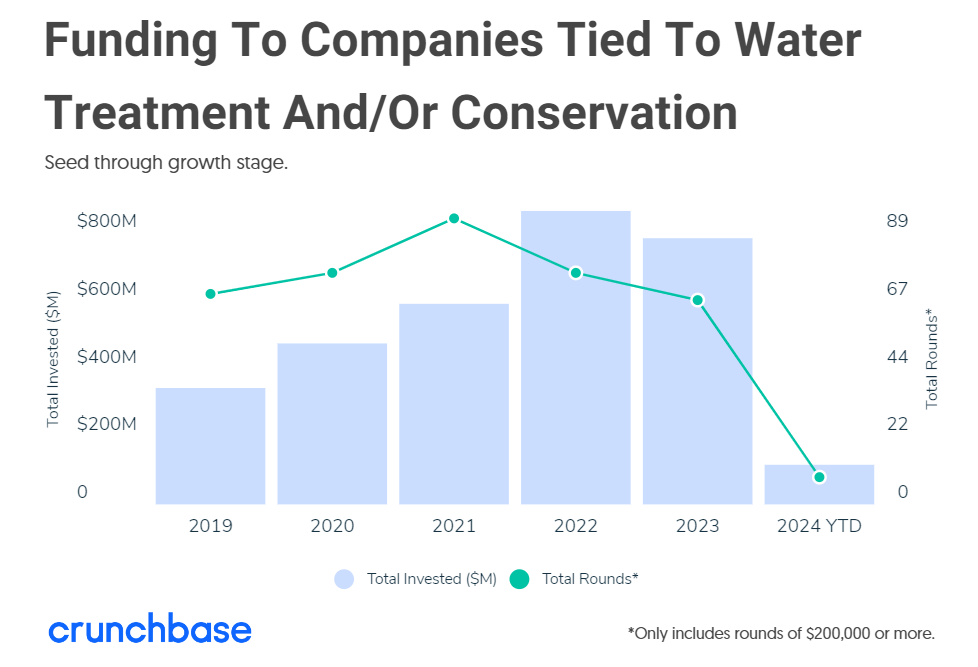

Context: In this downturn, VC investment amount in water tech is growing strong, since it’s underinvested in past years.

Total funding to water industry categories in 2023 was higher than in 2021. And this year is also off to a strong start. The annual investment since 2019 to companies in the water, water purification, and water transportation categories is charted below.

We believe that renewable energy will only displace fossil fuels if it’s price competitive with no subsidies. For example, both onshore wind and solar energy can compete with coal, but not offshore wind. Offshore is notably more expensive than onshore which is why it’s only a small fraction of total wind energy deployed. Orsted is the global leader in offshore wind, and it has been greatly impacted by the high-interest rate now. Cost is one of the top factors that decide if a new technology or product will survive. But in climate tech, the whole context is much more complicated than usual cost numbers. That’s why we need techno-economics analysis.

Questions to discuss in this panel:

ClimateTech Adoption must make economic sense, variables including Capex, Opex, regulation penalty, government incentives, downstream markets or off-taker agreements, even carbon credits, etc., how do investors evaluate if a ClimateTech startup has attractive economic?

How to validate the cost of a new ClimateTech such as carbon capture and hydrogen storage? (technology due diligence)

How can ClimateTech startups sell to large enterprises and shorten the sales cycle?

Case studies of techno-economics analysis with climate tech startups.

Moderator

Hani Elshahawi, Managing Director of NoviDigiTech – Hani is a thought leader in the energy industry, he has more than three decades of experience (18 years in Shell) in global operations, innovation, technology management, business consulting, and the full cycle of innovation from cradle to grave and from concept to commercialization in the energy industry with roles spanning technology, engineering, marketing, business, technology, and management. Before Shell, he had worked in another leading energy enterprise Schlumberger for 12+ years.

Speaker

Amy Henry, CEO of Eunike Ventures – Amy is the CEO/Co-Founder of Eunike Ventures and Lambda Catalzer, angel investor, TiE Houston board member, principal of TiE ATX LLC (Angels of Texas), and co-founder of Texas Innovation & Entrepreneurship Foundation. Amy was named by the Houston Chronicle in 2019, “Women Who Take the Lead in Building Houston’s Tech Ecosystem” (related to the launch of Eunike Ventures). Eunike was listed in 2022 as the ‘Top 6 Accelerators/Incubators Investing in Houston’ and the ‘Top 11 Best and Most Active Accelerators in Houston. Eunike Ventures, Inc., headquartered in Houston, Texas USA is a first-of-its-kind global energy venture builder /hybrid energy technology accelerator that works with innovative, technology companies through commercialization, across the entire Energy value chain. Eunike serves a unique gap in the global innovation system by bringing together energy companies, expert talent, and best-of-breed startups.

Sujatha Kumar, CEO of Dsider – Sujatha is an entrepreneur and senior technology executive, and is the Founder and CEO of Dsider. With a background in senior management roles at multiple technology companies in the energy sector, she notably led one of them to a successful sale to Honeywell. Sujatha and her team possess extensive experience in energy and industrial markets, focusing on mid to large enterprises.

About ClimateTech Investor Panels – This is for accredited private equity angel investors, venture capitalists, and corporate/institutional investors to share insights and investment opportunities and catalyze collaboration to help ClimateTech startups.

Hani: Although cost parity is crucial for the adoption of new climate tech, the reality is much more complex. Enterprise adopters are managing a systemic change, and new tech providers need to integrate their solutions into whole systems. Techno-economic analysis needs to build assumptions, sensitivity analysis, a process model, and history matching to validate simulations with real data. Enterprises look at the lifetime value of a new investment. When I evaluate climate tech startups for investments, I need to see they have already integrated themselves into their ecosystem and clients’ systems, not just presenting a single-point solution. And if their cost structure is higher than alternatives, even mature companies might struggle when some challenges emerge (for example, high interest rate), the recent Orsted cost crisis is an example.

Sujatha: Both large enterprises and startups need to build value stream mapping, system modeling, scenario analysis, risk analysis, and transition planning for a holistic analysis and simulation before new climate tech adoptions. There is so much data involved – operational, financial, and carbon abatement data and metrics need to be integrated, also domain knowledge is needed to assist with decision-making. We help both sides to make economic sense for net zero decisions and have supported the most disruptive climate tech startups.

Amy: How startups can best engage large corporations and shorten the time to commercialization and cash generation? Many climate tech startups offer innovations in materials or chemical reactions out of labs, and there is a big gap between a proof-of-concept or prototype and a pilot. They need to be able to design a pilot to convince large enterprises and investors. To prove the business use case is economically sustainable, data and simulation are important. They will need industry veterans with experience in integrating products and services as well as with the relationships with adopters to help facilitate technology trials with process safety in mind and minimal disruption to ongoing operations. The capabilities of handling large capital projects and integration planning are required. So for investors evaluating climate tech startups, looking for qualified and experienced talents in the team or partnerships, and for due diligence, you need industry experts to get involved.

Jessie’s note:

ClimateTech might be hyped now, but the reality is complicated. This session only gives a peek into what is needed in building and evaluating climate tech ventures. On top of innovation funnels, there are too many startups that have some new breakthroughs in the labs, they need lots more resources, talents, partnerships, and ecosystem adoption readiness, besides funding, to succeed.

To get to deployment, a technology must be completely de-risked, and ecosystem economics established so that every player in the value chain has a viable economic model. This means that managing a technology portfolio solely through the well-understood and widely used Technology Readiness Levels (TRL) stage gates is not enough.

Often, commercialization fails not because of the technology’s fundamentals, but because ecosystem economics have not been addressed or critical ecosystem players have not come on board. The economic and business model requirements for deployment, as well as a technology’s societal license-to-operate, can and should shape the technical problem definition and development of solutions at all stages of the RDD&D (research, development, demonstration, and deployment) continuum.

To describe adoption risks, the Office of Technology Transitions (OTT) has developed the Adoption Readiness Level (ARL) framework to complement TRL, and provided an assessment tool on the U.S. Department of Energy’s (DOE) website. It’s a very thorough picture of new technology adoption.

Also, another great resource from DOE is the Liftoff Reports. DOE’s Pathways to Commercial Liftoff reports provide public and private sector capital allocators with a perspective as to how and when various technologies could reach full-scale commercial adoption– including a common analytical fact base and critical signposts for investment decisions. The first Liftoff Reports are focused on advanced nuclear, carbon management, clean hydrogen, and long duration energy storage, Virtual Power Plant, Industrial Decarbonization.

Recommended resources:

Activate: Techonomics: Establishing best practices in early-stage technology modeling

Department of Energy: Techno-economic, Energy & Carbon Heuristic Tool for Early-Stage Technologies

China leads the world in energy transition investments (led by the state government and corporations). In 2022, China splurged more than 500 billion U.S. dollars into technologies like solar and wind energy, batteries, and electric vehicles. This was roughly four times more than U.S. investments. In 2021, European countries invested $219B in energy transition, about double the amount of what the US invested ($114B), according to the World Economic Forum. Of course, the Whitehouse has established the Inflation Reduction Act (IRA) in 2022 as a game changer. Furthermore, US startups received VC funding in ClimateTech more than in other regions – the U.S. received the largest share of global climate tech VC funding in 2022, at 41 percent. (according to Statista)

Interviewed by Jessie Chuang, the interview questions include:

Please introduce SWAN Impact Network (the most active impact investing angel group in the US).

Which nascent sub-sectors of climate tech have the most promising potential? (what sub-sectors are too crowded?)

How do you identify and evaluate them, and how do you do due diligence?

What are the risk factors for today’s climate tech startups? How do you de-risk them? The strengths of the US market?

What is your portfolio-building strategy in climate tech investing?

Takeaways:

SWAN was started in 2016 to invest in for-profit impact startups. The strength of the network is the deep experience of the angels in the network and their passion for helping our portfolio companies succeed. We work on a quarterly basis and we receive between 50-140 applicants per quarter from all over the US. We usually end up investing in 1-2 companies per quarter.

In a recent Climate Summit hosted in Houston, the good news is the IRA will pour around $1.2T into this space in 10 years, it’s not a cap, it’s a projection!

There are a number of different sub-sectors in climate tech that we believe are very promising. The first is improved efficiency, this will most likely be in electrical applications, but could also include things like ICE engines, industrial processes, water, construction, and building maintenance. Sometimes these interim solutions that will get us to an electrified future are overlooked. We also like solutions that combine innovations in hardware and software, giving us two potential technology moats. For example, solar or wind energies combined with AI/ML or algorithms could be promising. Lastly, we are excited by startups innovating inchemistry and material science that help remove carbon and/or produce more sustainable products. There are some areas we think are too crowded, including battery chemistry and carbon tracking software.

We have a relatively standard process that we use. We see a lot of startups that we meet at events or accelerators, are already engaged with one of our many partners, or apply to us directly. First, we make sure they fit our thesis and are in a stage that makes sense for us, and are raising an amount we think makes sense. We then add them to our process which starts with an introduction with one of us on the team and a review of their documents. We evaluate their impacts, financial return potential, deal terms, product-market fit, and most importantly the team.

How do we de-risk? The first is validation by customers, for example, they have paying customers, strategic partnerships, or at least a letter of intent (LOI). And if they have obtained government grants, that’s a very positive signal, since it’s non-dilutive funding with resources and expertise. Also, we can analyze investors – what other investors have invested, especially from potential future acquirers, even only a small amount. There are macro or market risks not controllable by startups, so the team is the most crucial factor, they must be competent to handle new challenges. Furthermore, we want to see the offering is so compelling, that it’s a must-have, not nice-to-have.

We mainly invest in US startups, because the US has a global influence, and governmental risk, market risk, and supply chain risk are minimized as much as possible in the US. But we’re living in a very global world, so we ask – how global is your supply chain? Do you have backups for your critical parts? Even if it’s not realistic for early-stage startups, it’s something you should consider when making investments.

Early-stage investors, either venture capitalists or angel investors, a portfolio-building strategy is needed – consider investing in 10-20 companies in 3-4 years because a lot of risks are unknown. It’s suggested to diversify across different sectors, geographies, genders, and backgrounds of founders, and add some companies without technology risks – the technology isn’t new, but the application or go-to-market strategy is novel.

About ClimateTech Investor Panels – ClimateTech is hard for investors not only because it’s mostly deep tech, but also because the variables for unit economics and adoption readiness are evolving. We interview one ClimateTech investor every Friday, a 30-minute Zoom meeting without live-streaming, we’ll do a briefing after every interview to be shared with broader networks. Join Zoom meetings to talk to speakers, or invite others to join the conversation/follow insights (Sign up).

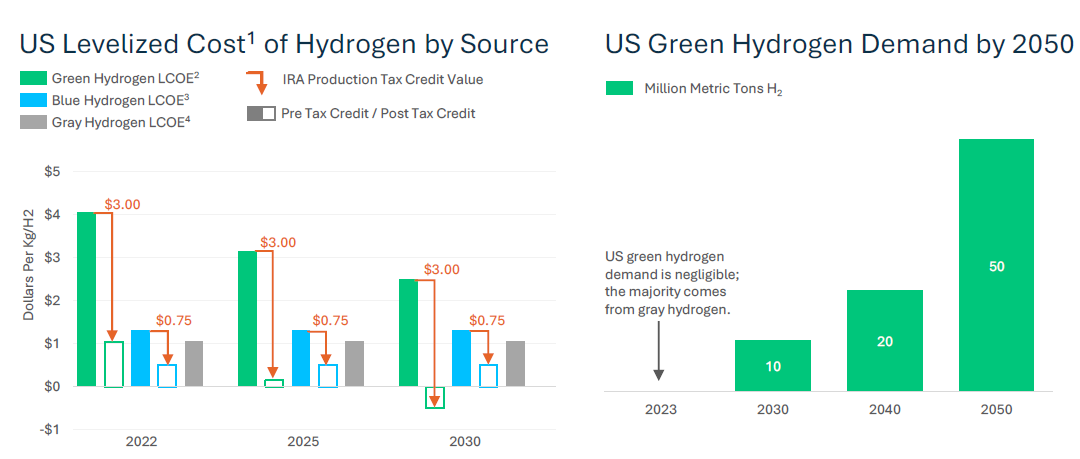

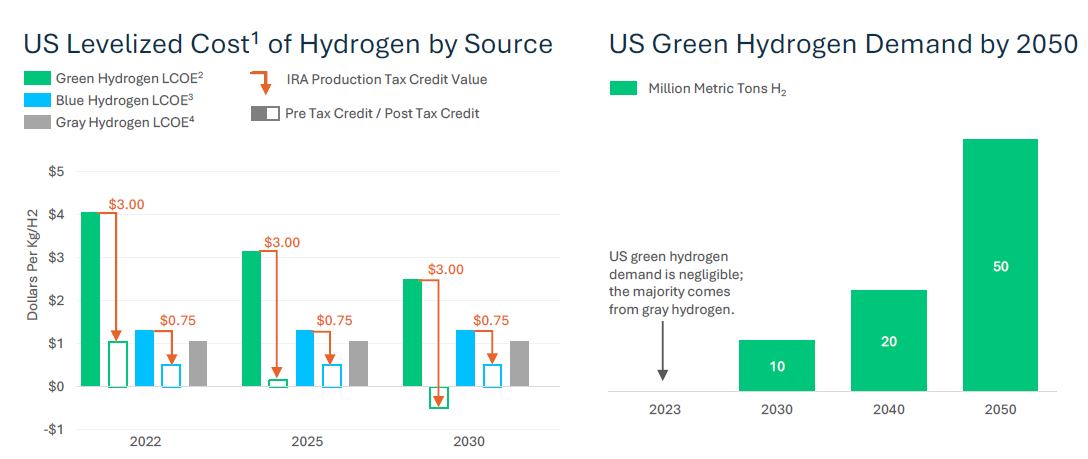

The climate crisis, the global clean energy transition, and the ‘electrify everything’ global movement are driving a massive transformation of industries and infrastructure globally. Green hydrogen has the potential to create a $1 trillion business and assist reduce more than 20% of the world’s CO2 emissions. The move to green hydrogen is being pushed by governments all over the world through new rules and incentive schemes.

Green hydrogen has been seen as the top decarbonization option for steelmaking, chemical manufacturing, and in fuel cells in medium to heavy-duty land transport. In aviation and shipping, besides replacing fossil-based vehicles with hydrogen vehicles, the EU also pushes for using e-fuel made from green hydrogen and carbon captured.

However, its high costs and the need for more infrastructure are the major hurdles. The IRA makes bold bets to unlock green hydrogen demand with production tax credits of up to $3 per kilogram. These incentives set the US up to be the cheapest source of green hydrogen in the world. For companies to qualify for the maximum tax credit, the law requires hydrogen to be produced with processes where the GHG emissions rate is less than 0.45 kg of CO2e per kg of hydrogen. For comparison, grey hydrogen produces about 24x more CO2e. Furthermore, the DOE has allocated $8B to develop six to ten regional hydrogen hubs across the US.

— From The Future of Climate Tech, June 2023, by Silicon Valley Bank

Besides subsidies, many companies are working to develop technology that can reduce the cost of clean hydrogen. especially electrolysis technologies. The two main commercial hydrogen electrolyzers currently dominating the market—Liquid Alkaline & PEM—either have low efficiency or are extremely expensive. One technology of particular interest is AEM (anion exchange membrane) electrolysis technology. AEM technology is an innovation focus area because of heap CapEx and lower OpEx with higher efficiency, and its potential to integrate directly with intermittent renewable electricity while using low-cost abundant materials.

Electrolyzer companies that have reached commercialization and are manufacturing 100s of MWs of electrolyzers are typically worth over $1B (Plug Power, Nel, Nucera). Pre-commercial electrolyzer companies with a certified, 1MW+ system design have received valuations of $200M+ (Ohmium, Electric Hydrogen, Enapter, H-Tec). Of course, there are a lot more upstart challengers working on similar technologies. No need to chase startups with hyped valuations.

We are seeing more emerging startups addressing challenges in the green hydrogen economy or building new innovations. Some examples:

New membrane-free hydrogen production technology reduces CapEx by half compared to traditional electrolyzers with higher energy efficiency.

Hydrogen purification is needed for all kinds of hydrogen generation methods, better performance and the same or lower cost is pursued.

Hydrogen dispensing/fueling infrastructure is the biggest gap to support vehicles with hydrogen fuel cells. Companies offer on-site or off-site hydrogen generation, compression, and dispensing appliance uses water and electricity to produce high-purity fuel cell-grade hydrogen, powered by renewable power. There are different solutions serving the trucking industry or consumers.

The efficient storage of hydrogen onboard trucks, ships, and planes remains one of the key challenges. Startups take the challenges of the existing hydrogen storage solutions to improve volumetric density, weight, safety, and cost. Also, a startup enables hydrogen to be stored within an organic liquid which can be handled and transported no differently than gasoline.

Producing green hydrogen and biochar from agricultural waste streams, and monetizing the carbon credits the activity generates. More than 30% of U.S. total methane and 70% of nitrous oxide emissions come from the decomposition of agricultural wastes (from DOE), this process solves it at the same time while producing green hydrogen.

Producing carbon neutral high purity hydrogen from recycled feedstocks such as plastics and tires.

Using microbes to make hydrogen from oil, the team backed by Occidental Petroleum claimed they can produce hydrogen at $1 per kilogram by injecting oil-eating microorganisms inside depleted crude reservoirs.

A hydrogen marketplace makes it easy to trade and procure hydrogen.

A capital-light approach to hydrogen logistics by transporting green hydrogen in modular capsules over the existing freight network from green production sites to airports around the world, plus conversion kits to retrofit the existing fleet with a hydrogen fuel cell powertrain.

Repurposing old fossil fuel reservoirs as sources of clean hydrogen, harnessing biological processes to convert leftover hydrocarbons from subsurface wells into usable hydrogen while capturing and storing CO2(use other microbes to lock it underground). This is called Gold Hydrogen.

Join us for more discoveries and discussions on investment opportunities and risks in the green hydrogen economy.

Harvard Business Review had done a survey and interviews with the vast majority of leading VC firms. Specifically, the team asked about how VCs source deals, select and structure investments, manage portfolio companies post-investment, organize themselves, and manage their relationships with limited partners. There were responses from almost 900 venture capitalists — making the study the most comprehensive to date.

They found that…

Even for entrepreneurs who do gain access to a VC, the odds of securing funding are quite low. Our survey found that for each deal a VC firm eventually closes, the firm considers, on average, 101 opportunities. 28 of those opportunities will lead to a meeting with management; 10 will be reviewed at a partner meeting; 4.8 will proceed to due diligence; 1.7 will move on to the negotiation of a term sheet with the startup; and only one will actually be funded. A typical deal takes 83 days to close, and firms reported spending an average of 118 hours on due diligence during that period, making calls to an average of 10 references.

Though VCs reject far more deals than they accept, they can be very aggressive when they spot a company they like. Vinod Khosla, a cofounder of Sun Microsystems and the founder of Khosla Ventures, told us that the power dynamic can quickly flip when VCs become excited about a start-up, particularly if it has offers from other firms.

As the investment climate has turned investor-friendly this year (2023), this panel will interview VCs about how their investment funnels and decision-making process are structured, with a focus on deep tech startups.

Topics:

Introductions of Lam Capital/Research, SOSV, TINVA, Ceres Capital and their missions and stages of startup engagement/investment

The process of deal sourcing, evaluation, due diligence, decision-making, negotiation and more in different VC firms

The most important considerations and their priorities for decision-making in different VC firms

A good company and a good deal, what’s the difference?

The involvement and exit strategies after investing in startups

The prioritized innovations/solutions you are looking for from startups now

Advice for deep tech startups to build a relationship with you as well as fundraising preparations

Whether you are an entrepreneur or an angel investor, if you are interested in joining the conversation, and asking your questions to the panelists, including feedback on your startup, market insights, etc., sign up here. This is an invitation-only event. If you sign up, you can ask questions, and no matter whether you join or not, we’ll send you the meeting summary.

Speakers

Alexander Hall-Daniels – Alex is a program manager and had been a senior analyst with SOSV IndieBio’s New York office, a VC investment firm operating within biotechnology and life sciences. He has a diverse, global perspective cultivated from the wealth of international professional and educational experiences across the US, UK, and the rest of Europe.

Mike Huang – Mike is an investment manager with Lam Capital (Lam Research CVC), focusing on semiconductor manufacturing startup investments now. previously he has worked with Amazon, Samsung Electronics, and TSMC. He has an educational background in technology management and MBA from Taiwan and UK.

Yvonne Chen – Yvonne has over 20 years of success in telecom, security, MedTech, and early-stage investments and operations, including handling corporate investments at MICROELECTRONICS TECHNOLOGY INC., CDIB & PARTNERS INVESTMENT HOLDING CORP., H&Q TAIWAN CO., HTC CORPORATION, WI Harper, and Infinity Ventures. She has strong industry expertise and connections in Taiwan, Greater China, and Silicon Valley.

Jessie Chuang – Jessie is a startup advisor with US and international teams, a judge with Unicorn Battle and MassChallenge, an angel investor with several US angel networks, and an emerging venture fund manager. Her previous experience includes 10+ years in semiconductor R&D and team management at UMC, and another 10+ years in corporate consulting on digital transformation working with executives.

About TINVA

TINVA (Taiwan ITRI New Venture Association) is a Non-Profit Organization startup facilitator and venture builder that partners with various deep-tech stakeholders in order to provide startups with the resources, mentors, tools, and support needed in order to succeed. TINVA is associated with the top deep-tech research institute ITRI backed by the Taiwan government – the top source of deep-tech startups and innovations in Taiwan.

About Global League

Global League is an investor partnership with augmented collective intelligence built from a process proven by top angel networks with an average IRR >25% and 330+ exits. We connect quality investment opportunities from top US angel networks and VCs and collect intelligence from co-investing fellows.

About Founder Institute

The Founder Institute is the world’s most proven network to turn ideas into fundable startups, and startups into global businesses. Since 2009, our structured accelerator programs have helped over 7,000 entrepreneurs raise over $1.75BN in funding. Based in Silicon Valley and with chapters across 100 countries, our mission is to empower communities of talented and motivated people to build impactful technology companies worldwide.

About Wise Ocean

Wise Ocean builds up a global network to connect proven startups or scaleups, industry leaders, corporate innovators, ecosystem partners, and investors for impact and profit-making. For international startups entering the US market, we will help navigate US resources (partners or accelerators) matched to your needs, for US companies looking for Asia manufacturing or market partners, we have several partners that can help, such as TINVA.

This website uses cookies to improve your experience while you navigate through the website. Out of these cookies, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may have an effect on your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.